The Demand Side of Vertical AI

Capital Efficient #12

Welcome to the latest edition of Capital Efficient. This one is a little different — a single long essay instead of the usual deal roundup and reading list. We’ll be back to the regular format next issue.

The Demand Side of Vertical AI

Something is shifting in vertical AI that the mega-rounds in AI-native platforms and AI services businesses miss. The most interesting thing about AI is not the competition it enables — it’s how AI expands which markets exist.

Over the last few years, I underestimated how fast frontier models would match trained professionals in their quality of output. I also underestimated how broad the categories of expertise would turn out to be. As an investor, I had one perspective, but after getting more hands-on building with these tools my sense of possibility has changed. This spring I spent a few days rebuilding a community health navigator for a New Haven clinic that had lost its federal funding for navigator roles. That small project was enough to change my read on where things are heading.

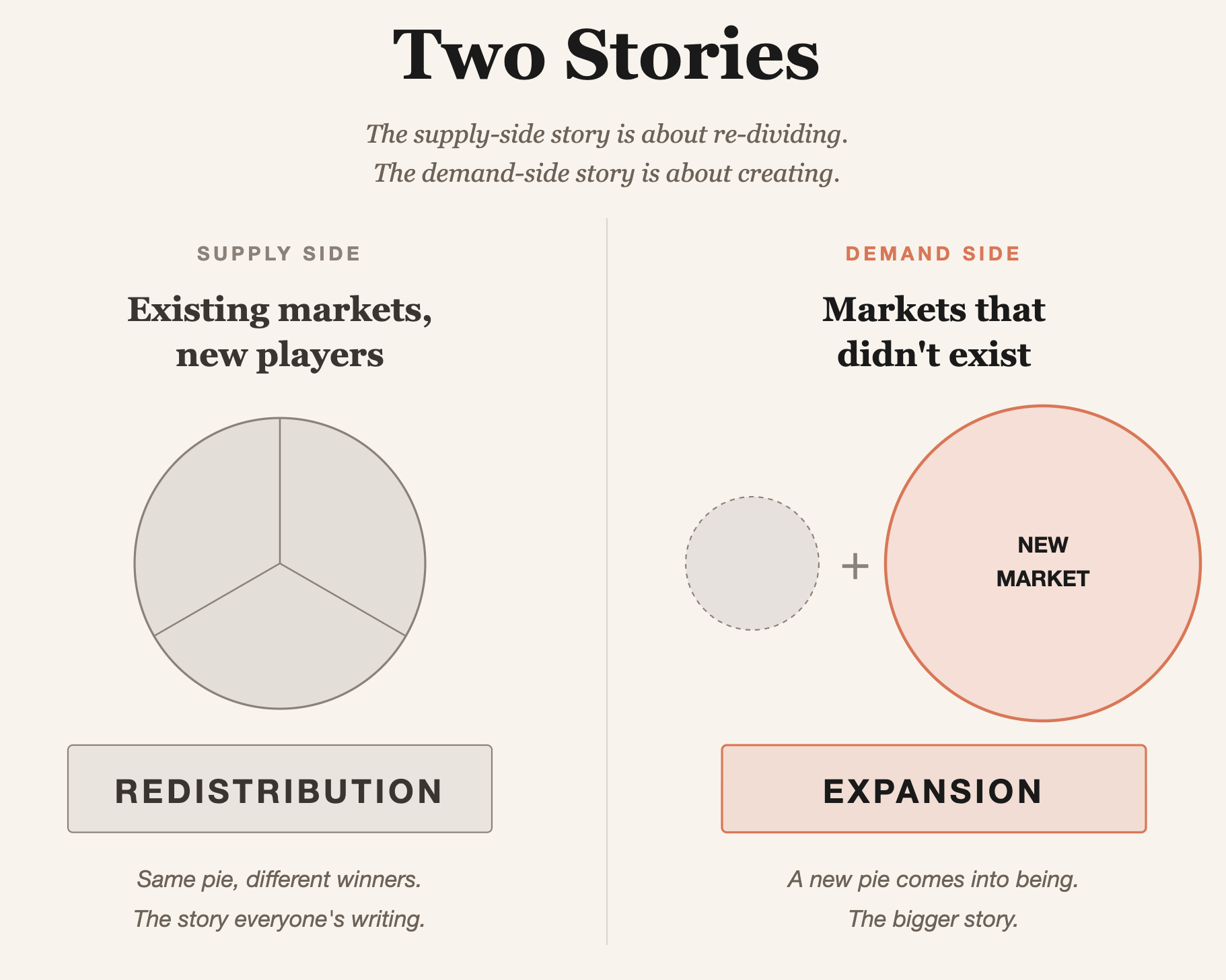

To borrow from Gibson: what I’d call AGI-ish is here; it’s just not evenly distributed. Most of the analysis I read, including my own, is still sorting which $50B legacy markets get re-divided by which AI-native entrant. That analysis isn’t wrong, but it’s only a part of the discussion.

The more pressing question is which markets come online at all, and what kinds of companies form to serve them. That’s the demand side.

What the Supply-Side Story Misses

Let’s start with the supply-side consensus, because everyone reading this is likely already fluent in it.

Vertical SaaS is under threat as a category. The moats that justified venture-scale outcomes — enterprise-readiness, workflow IP, integration surface area — are collapsing into the model layer. The thing the software used to do, the model can now do. The thing the model can’t yet do, a small AI-native team wraps around a foundation model and ships in a quarter.

As a result, many investors are pivoting towards backing AI-native services businesses that eat the workflow end-to-end and provide a managed service offering to an end-user instead of an efficiency platform. Crosby for legal work, Hanover Park for fund administration, Corgi for business insurance, and many more like them launching every week. The playbook is straightforward: don’t sell the tool to the professional — be the professional, at 10x the leverage and a fraction of the cost. I wrote about this in Five Approaches to Vertical AI. It’s accurate — but it’s also the part of the story everyone else is writing. Amidst this technology shift, workflow automation is most at risk. The best companies in that bucket are evolving: into platforms of record, or directly into AI-native operators competing with the customers they used to sell to. Those that stay tools get subsumed by the model layer.

The Bigger Question: Demand-Side Expansion

It’s clear we now have near-infinite affordable intelligence on tap. So how does that impact customer demand?

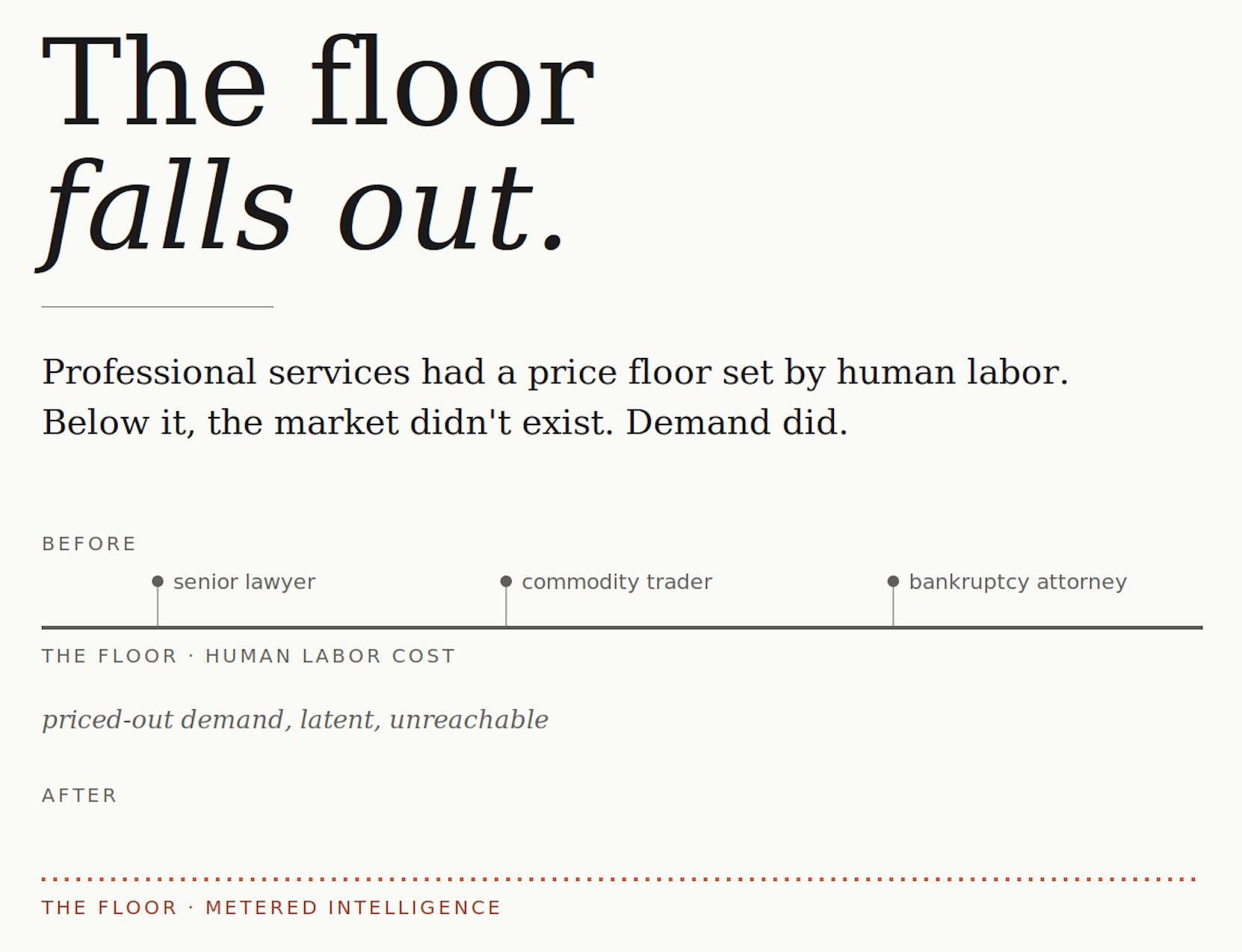

Professional services have historically had fixed minimum price points set by human labor costs. A senior lawyer. A commodity trader. A Medicare enrollment counselor. Each had a compensation floor, and the floor excluded entire categories of buyers. SMBs couldn’t afford the lawyer. Regional distributors couldn’t afford the trader. Underfunded clinics couldn’t staff the counselor. Demand was always there but the unit economics were not. AI collapses this compensation floor and can meet latent demand that had previously been priced out.

So what does this look like? Three illustrative examples:

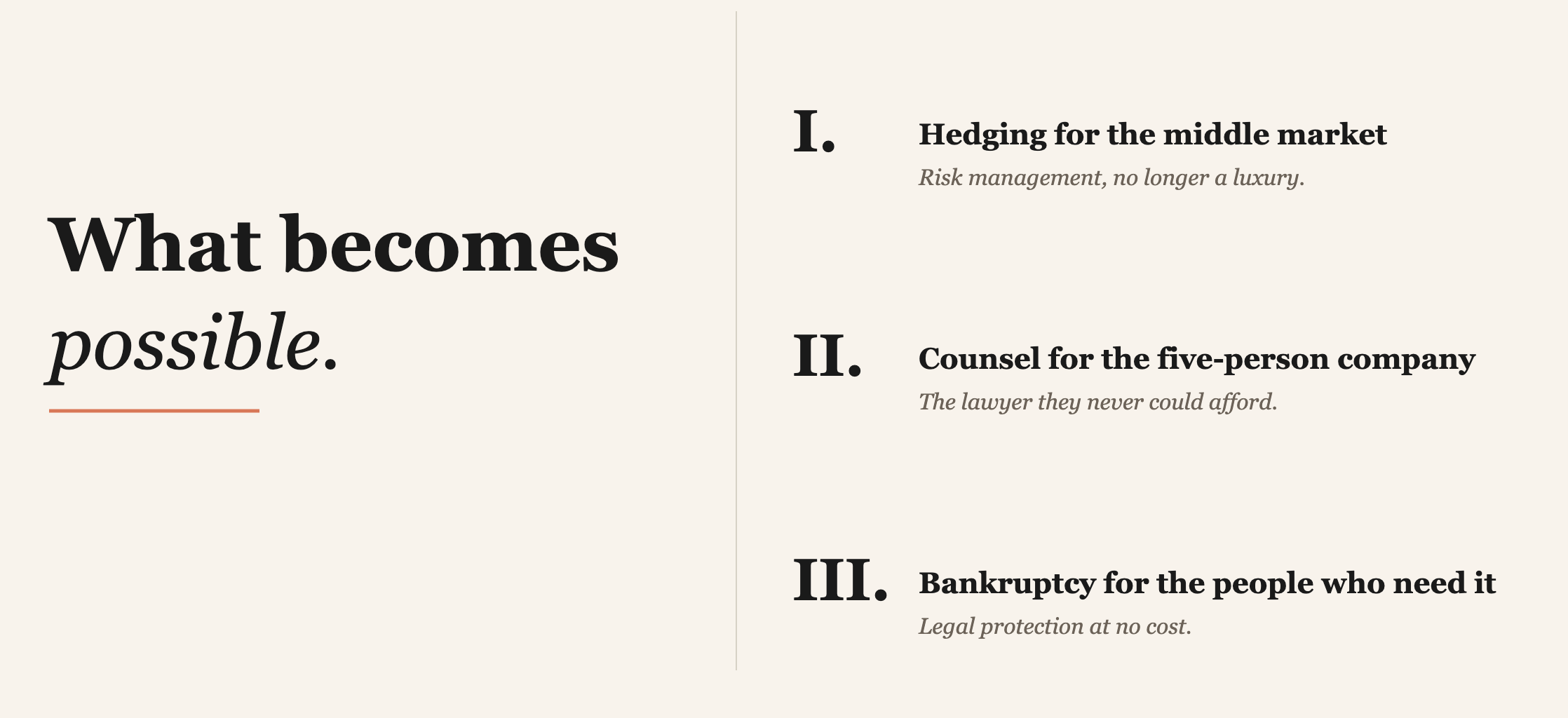

Commodity hedging. An airline or an agricultural giant — think Delta or Cargill — has commodity traders on staff. A regional food distributor doing $200M in revenue does not. It can’t afford to hire away a Wall Street senior trader, it doesn’t have the FCM relationships, and it can’t hit the bank desk minimums. So they don’t hedge. The market, at their scale, didn’t exist. Pillar raised a $20M seed this month led by Andreessen Horowitz to solve exactly this. Their platform automates hedging for commodity-driven businesses — metals recyclers, import-export firms, food traders — at a price point the old desks couldn’t touch. The founder, a former macro trader, put it plainly: “Sophisticated institutions had access to tools, infrastructure, and talent, while the actual producers, importers, and manufacturers driving global trade had little to no access. Risk management was treated as a luxury, despite being essential…[o]ur goal is to make hedging as accessible and ubiquitous as payments or accounting software.” The market for hedging had priced these companies out of the discussion — but now this is a service that’s been made accessible to the long tail of hypothetical customers.

Legal access for small businesses. Everyone understands “I can’t afford a lawyer.” A five-person company with a contract dispute, an IP question, or a vendor who won’t pay faces a $5,000-$15,000 minimum engagement at any real law firm. Most never engage. They eat the loss, sign the bad contract, and Google their way through it. An AI-native legal service that drafts the demand letter, reviews the MSA, or files the motion doesn’t need to replace the lawyer. It needs to exist at a price point where the small business picks up the phone, with this new service becoming the lawyer they never could afford. That small business wasn’t a client of the legal industry before. Now it is.

Bankruptcy access for low-income Americans. A typical Chapter 7 filing can cost over $2,000 in attorney fees — money the people who most need bankruptcy protection don’t have. Legal aid is overwhelmed, and most eligible filers never even file. They live with the debt instead. Upsolve, a 501(c)(3) non-profit, built a free AI-native self-filing tool that has helped more than 16,000 families eliminate over $1B in debt. A consortium of foundations has been funding Upsolve Assist, an AI financial counselor that analyzes individual situations and provides personalized debt-management guidance at no cost. It isn’t a cheaper bankruptcy lawyer — it’s a new shape of legal service the old unit economics didn’t allow. The families that Upsolve serves couldn’t access these kinds of legal or financial advisory services before. Now they can.

Demand-side expansion comes in two flavors:

On one end: existing services reaching buyers who were always excluded. On the other end: categories of organization that were never economically feasible before, now becoming viable — a three-engineer shop shipping AI tools for a hundred under-resourced clinics, AI hedge funds for the middle class, social services navigation for cities that lost their federal funding. AI’s ability to bring metered on-demand intelligence to any problem is the commonality across these ideas.

The further out you go, the more interesting (and weirder) the companies can get — and the less the existing industry even recognizes them as competition, because they’re serving a previously unaddressable market segment.

The pattern itself isn’t new. Clayton Christensen’s non-consumption framework gets at this: when the cost floor drops, markets that were always there become reachable. What’s new is the speed, the fact that distribution becomes the moat rather than technology, and the kinds of companies it enables.

A View From One New Haven Clinic

Federal budget changes last year cut the community health navigators at a clinic in New Haven — the people who help under-resourced patients find health, housing, food, and immigration services. The funding stream that paid for the navigator role dried up, but the need did not.

I spent a few days and built the clinic a live bilingual navigator with 192 local resources, routing by need, and a simple tracker — enough to prove the bottleneck wasn’t engineering talent but whether anyone would build the thing at all. I’m not launching it in this piece, but it did clarify something for me. The hardest unsolved problem in AI isn’t capability. It’s whether the model ever reaches the clinic.

Writing the software was the easy part. The hard part was the question I kept running into at every step: who does this actually reach, and how? A front-desk volunteer? A bilingual community organizer? A link shared in a WhatsApp group? I haven’t solved this. That’s the point. The engineering was trivial. The reach problem is the actual work, and the essay you’re reading is partly me admitting I don’t know the answer yet.

The version of the story that works is one where this kind of tool becomes the default for under-resourced institutions — not because someone builds it for them centrally, but because the unit economics of building it have collapsed to the point where the tool gets built locally, by one person, in days. That’s the far end of the spectrum I described above. Not an existing service reaching a new buyer. A category of organization that had no business model before, with one now.

A non-profit development shop of three to five people, serving 100 under-resourced institutions at a time, is now a viable organization. The same logic applies to clinics, community colleges, small municipalities, legal aid offices — the parts of the public and social sector running on donated time and grant cycles. Whatever shape the for-profit operators take, someone also needs to build the version that serves populations the commercial version was never going to reach.

The tool only exists because the primitive underneath it is cheap, reliable, and accessible enough for one person to build on in a weekend. That’s not guaranteed. That’s a lab decision.

Timing, Distribution, and the CAC Problem

The timing is unusual. Most technology transitions go: incumbents die, then new things emerge in the wreckage. This one is different — new markets are forming before old ones finish dying. Demand is moving faster than displacement, because the bottleneck was never supply. It was the buyers who were excluded from the market in the first place. Create intelligence cheap enough, and the excluded buyers become customers immediately. Incumbents take longer to unwind than new markets take to form.

The moat is distribution, not technology. The real defensibility for the companies at the far end of this expansion isn’t the AI — it’s being the first to build go-to-market for populations no one has ever sold to. Pillar doesn’t just automate hedging; it invents the sales motion for metals recyclers who’ve never bought a financial product. A non-profit dev shop doesn’t just build tools for small clinics; it earns credibility with administrators who’ve never deployed AI. Technology is becoming a commodity. The relationship with the underserved buyer is the asset.

The risk. The sharpest pushback is predictable: SMB acquisition cost is the real ceiling. You can’t acquire a $30/month customer for $1,000 and build a venture-scale business.

Two responses. First, when you’re being the service rather than selling a tool for it, revenue per customer is structurally higher. A SaaS tool charges $50-200/month. An AI-native service doing the actual work — the legal filing, the hedge, the staffing, the benefits enrollment — charges on the value of the output. Revenue per customer is 5-20x higher. CAC math changes when the revenue line changes.

Second, and more honestly: CAC itself is a distribution problem that’s been unsolved for thirty years across CRM, cloud, and fintech — not because no one tried, but because the cost lives in trust-building, not lead generation. Fragmented buyers, no procurement infrastructure, long sales cycles relative to contract value. AI changes the revenue side of the equation. It doesn’t automatically change the trust side. Which is why the deployment-reliability question I’ll get to at the end of this essay is so important: it’s the mechanism by which acquisition costs actually come down over time (or don’t).

The supply-side story is about which $50B markets get re-divided. The demand-side story is about which human interactions (and businesses) become possible for the first time.

What Would Prove This Wrong

Three things that could prove me wrong:

Frontier model plateau — if frontier models stall out (which is not a bet I would take given the last 24 months), AI doesn’t get reliable enough to bring these new organizations into being.

Agentic reliability — if AI can’t move past the last mile of “plausible but wrong,” copilots survive but full agents don’t due to a lack of trust. Again, not a bet I would take.

Regulatory capture — law, healthcare, and finance are the biggest excluded-buyer categories and also the easiest for incumbents to lock down with licensure rules. Watch state bars and insurance commissioners in 2026-2027.

The popular falsifier — enterprise-readiness — is a speed bump, not a moat. Models keep eating it.

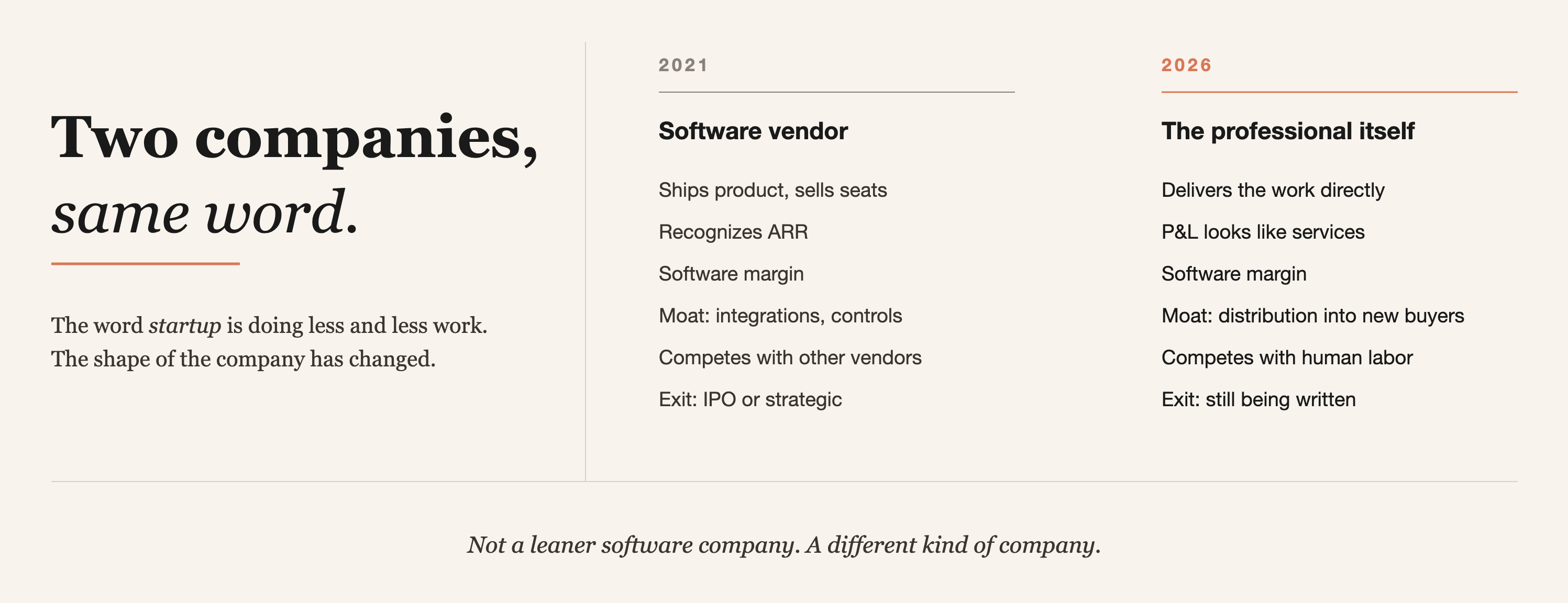

What a Startup Even Is Now

Which is why the word “startup” is doing less and less work.

The venture-backed company of 2021 was a software vendor. It shipped a product, sold seats, recognized ARR, and defended a moat built out of integrations and enterprise controls. Five to ten years to $100M ARR. Exit path either public market or strategic acquirer. The venture-backed company of 2026 is something else. It doesn’t sell software to the professional — it is the professional.

Its P&L looks like a services business, while the company tries to make its margin structure look like software. Its moat is distribution into populations no one has ever sold to. Its competitive set is not other software vendors — it’s the labor pool of humans doing the work today, at a cost structure that excludes a whole swath of potential buyers the company could otherwise serve.

The key difference: it’s not a leaner software company — it’s a completely different kind of business.

And the shape keeps shifting. A single immigration attorney running 500 active cases. A boutique M&A advisor doing sub-$10M deals the big banks won’t touch. A two-person firm managing 10,000 rental units. A patent-filing shop that replaces a $2M/year associate team with one partner and a model. None of these are “startups” in the 2021 sense. They’re a new class of organization, and the commentary hasn’t caught up.

The playbook for founders: stop benchmarking yourself against SaaS. Your comp set is incumbents writ large — the law firm, the brokerage, the consultant — not Salesforce. Your hires are engineers plus domain operators, not engineers plus product managers. Your board wants people who ran a business in the vertical, not more software executives. Your fundraising story is about creating a market and capturing services margin, not ARR growth at 120% NRR. The faster you stop pretending to be a SaaS company, the faster the P&L starts making sense.

The question I’d ask any founder right now: are you building the 2021 startup or the 2026 one? The difference is not incremental — and the market will eventually tell you which you are.

The Constraint Is Reach

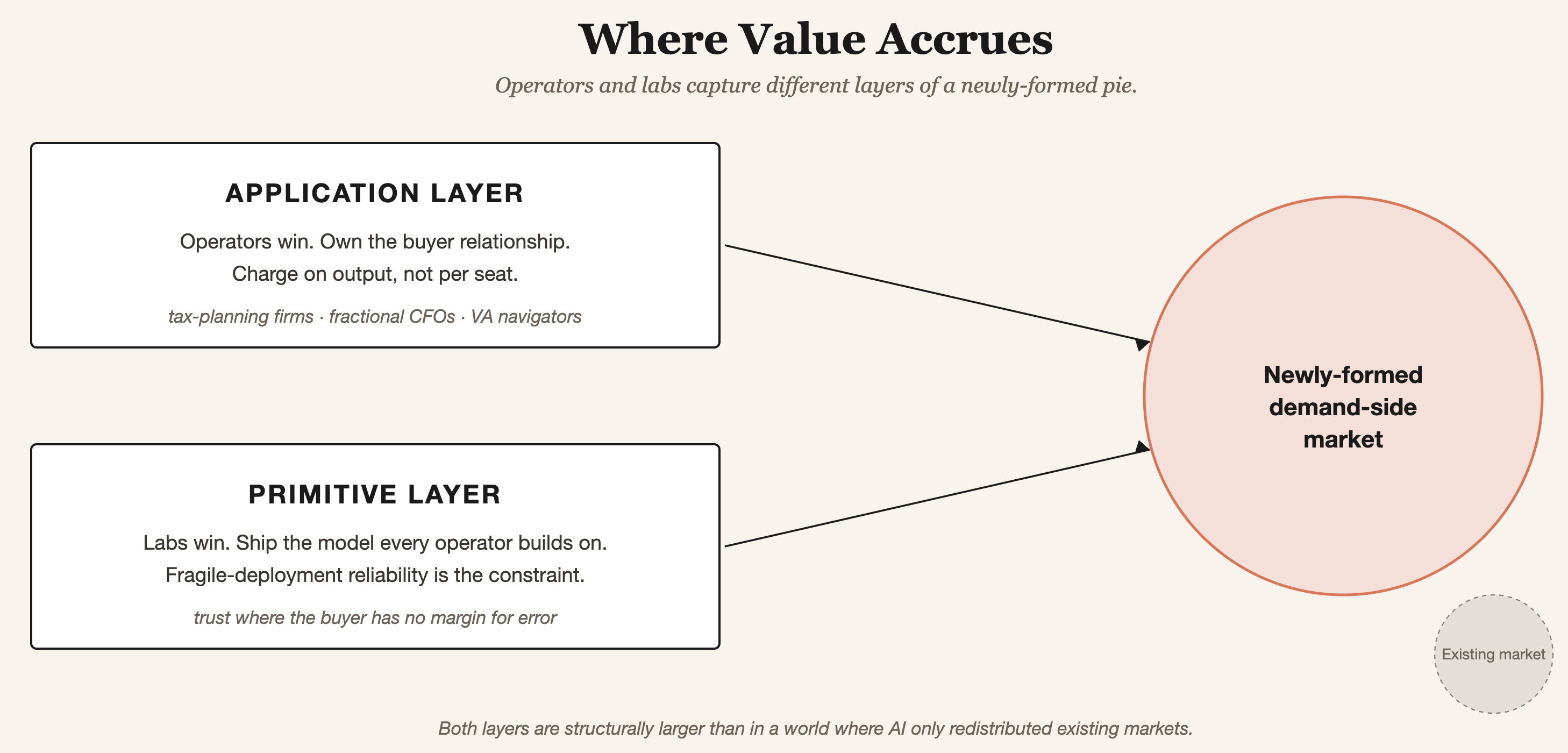

If the demand-side expansion is the real story of the next decade, value accrues at two layers at once.

At the application layer, operators win. They own the buyer relationship no one else has ever built. The tax-planning firm for doctors and dentists priced out by family-office retainers, the fractional CFO for $10M-revenue companies who couldn’t justify a full-time hire, the VA benefits advocate for veterans waiting years on their claims — each becomes indispensable infrastructure for a buyer the existing market wasn’t built to serve.

At the primitive layer, the lab that ships the model every operator builds on captures the largest share of a pie that just got much bigger. Not because the lab won the existing market — because the market it’s serving is the one the existing offerings couldn’t reach.

Those aren’t in conflict. They’re complements. The demand-side expansion creates a newly-formed pie. Operators capture the application layer of it. Labs capture the primitive layer of it. Both layers are structurally larger than they would be in a world where AI was only redistributing markets that already existed.

The obvious tension: labs have repeatedly moved up the stack. Consumer chat products, agents, vertical assistants. If labs capture application-layer value directly in the categories I’m describing, the operator thesis narrows. My bet is that the deployment contexts that matter most here — asylum hearings, title objections, Medicaid enrollment — are the ones labs are least equipped to own, because they require vertical trust-building labs aren’t structured for. But that’s a bet, not a foregone conclusion.

Where the primitive layer gets interesting is that the deployment context for demand-side expansion is unlike the context frontier labs optimize for by default. The asylum applicant can’t tell whether a misworded pleading will cost her the hearing. The solo inventor can’t evaluate whether the claim language the model drafted leaves his IP exposed. The first-time home buyer can’t know whether an AI-drafted title objection actually protects her deposit. Trust at the point of deployment is the entire product.

The difference between labs stops being what shows up on an MMLU leaderboard. It starts being whether the lab is investing in silent-failure detection in populations who won’t push back when a model gets it wrong. If the failure is invisible to the lab, it never gets fixed — and if it never gets fixed, the whole category of deployment stalls at the populations who most need it.

This is also the CAC answer from earlier. Distribution into excluded populations is expensive because trust is expensive. Silent-failure detection isn’t a lab-ethics problem — it’s the mechanism by which acquisition economics eventually work, because a service that quietly fails on the populations it claims to serve never builds the reputation that lowers CAC over time.

Not every lab is trying to win this game. Some are optimizing for reach and consumer attention. Some are optimizing for benchmark dominance. A smaller number are treating fragile-deployment reliability as the entire product.

If AI is going to expand which markets exist, that is the constraint that matters. Not whether the model is impressive in isolation, but whether it can be deployed where trust is thin, feedback is delayed, and the buyer has no margin for error. And when that happens, what kinds of businesses become possible?

The power law is going to be even more pronounced for the AI age. That's why frontier model intelligence won't be the bottleneck. Distribution and productization will.

Flagging a related podcast - Pat, you might like this one:

https://cloudreturns.cloudratings.com/episodes/pat-mcgovern-bowery-capital-where-vertical-ai-wins

https://youtu.be/ccjYlNIhhus