Deployment Is All You Need

Capital Efficient #13

Welcome to the latest edition of Capital Efficient. Let’s get into it.

Software and services are converging, and the companies that used to sell one are about to compete with the companies that sold the other. A brokerage, an agency, a back office: each now faces a competitor that would have shipped as a software product three years ago. Meanwhile the software founder building for that vertical looks less like a SaaS vendor every quarter and more like an operator. The line between selling the tool and doing the work is basically gone.

So if you’re in a vertical, you have one decision to make: what are you actually going to be?

You can be the industry’s AI operations partner. Hand them a platform that brings AI into their business off the shelf, or run the vertical BPO and let them keep doing what they do. Or skip the partnership entirely. Don’t sell software to the industry. Become a participant in it.

What’s Actually Defensible

Four shapes worth building, on a spectrum from “we are the industry” to “we sell the industry one discrete thing.”

Direct competition. You’re vertically integrated. You don’t sell software to law firms or trading desks or pest control operators. You are one, built AI-native from day one, with a margin profile the incumbents you’re eating can’t match.

Software plus services, heavy FDE. You build custom automation platforms for an industry with a forward-deployed motion (I’ve written about this before). The old wisdom said the custom dev shop was a death sentence: unfocused, unscalable, every deal a snowflake. That wisdom is dead. When the cost of producing a feature collapses, the snowflake problem collapses with it. You no longer need one rigid wedge. Throw the whole menu on the landing page and see where they bite. If you can pay for it, we can build it.

The human-centric play. Keep humans in the industry and arm them to go out on their own: business-in-a-box plus AI for the SMB and mid-market broker, agent, trader. The catch is that a pure workflow tool is something they can eventually rebuild. So you need a network effect or a shared cost center underneath it, pooled sourcing or procurement or distribution, something that compounds as more people join and won’t clone in a weekend. Aim it at an industry with no intention of building its own tech.

Discrete AI services. I do the one thing you don’t want to touch and sell it back to your existing customers. Commodity hedging. Leads for the pest control business. Ad campaigns across every platform. The compliance function nobody wants to own. Your customers were already paying an agency or a consultant for this. Now you do it AI-forward, at better margin, as a better product, to the same buyers.

All four rest on one assumption: AI takeoff keeps going. Bet accordingly.

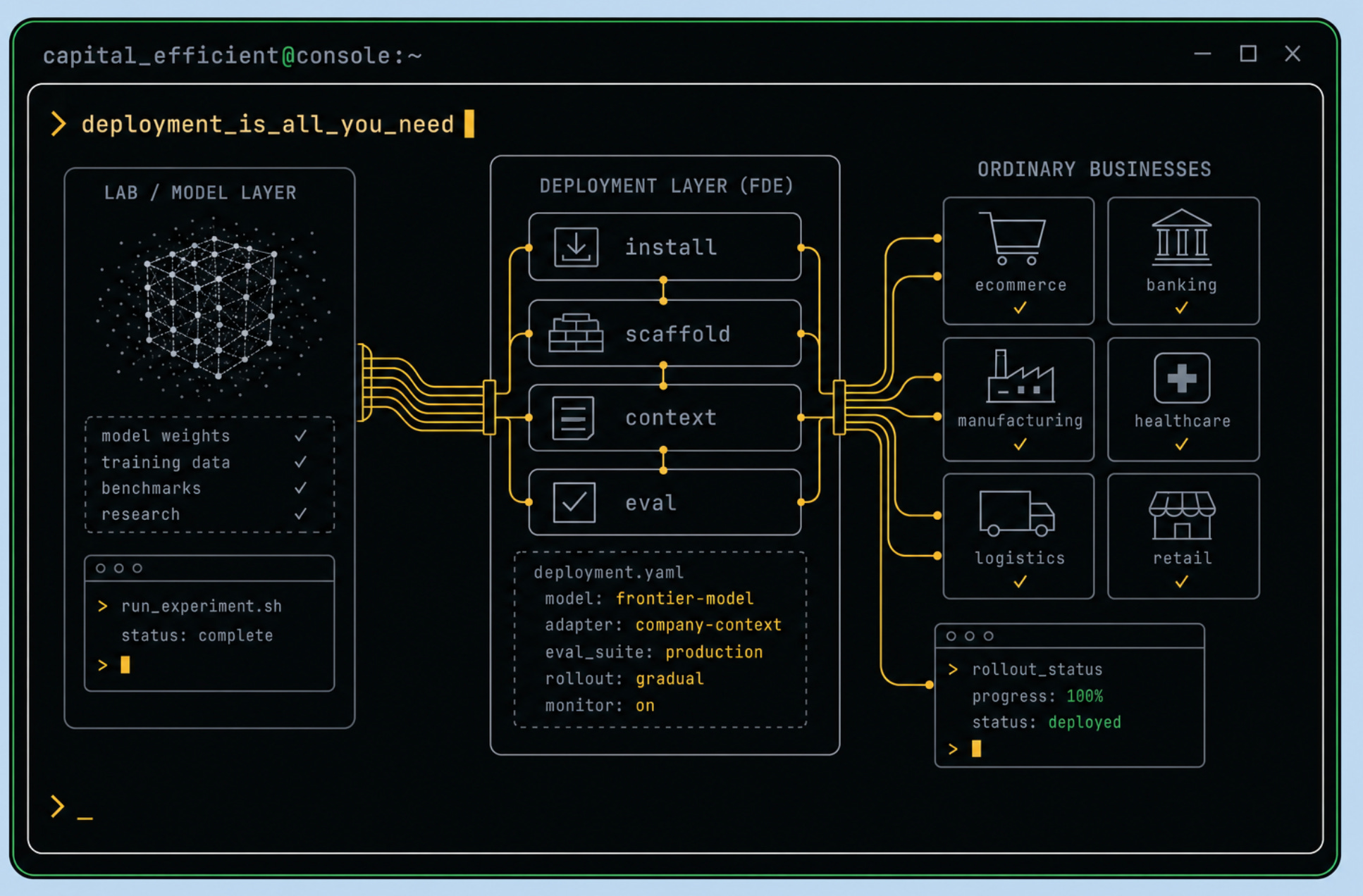

Deployment Is All You Need

What I’d call AGI-ish is already here. It’s just not evenly distributed.

Tech lives inside a bubble of its own perception. Most companies still won’t let Claude Code near a codebase, run IT locked down to the studs, and employ people who have never used AI past a chatbot conversation. Meanwhile the models are AGI-ish at certain functions, provided someone builds the scaffolding and context and evals around them. Most companies can’t build any of that in-house. They don’t have the people, they won’t for years, and without a catalyst most won’t even try.

That gap is the whole opportunity, and it gets captured three ways.

The transformation shops walk into the non-tech economy and wire this stuff in. My view: the great fortunes of this cycle get made the way they got made in the ’90s, when SAP and Oracle shipped the software and Accenture and Deloitte got rich installing it. They resold and configured what others invented. And the engagements quietly grow a maintenance tail (recurring configuration, upkeep, evals that need tending) that starts to look like ARR. We’ve come all the way around.

The challengers skip the incumbent entirely and compete with him. Look at what Sequoia is funding: SendCutSend (on-demand parts manufacturing, $110M at a $1B valuation), Crosby (an AI-native law firm, not legal software), WithCoverage (an AI insurance brokerage). These are companies built to compete inside large industries rather than software sold into them, on the thesis that an AI-native entrant scales fast in categories that were always too labor-heavy to interest venture. The margin profile that made professional services un-fundable is precisely what AI rewrites.

And AI-native PE buys the incumbent and transforms him by force. It has the people to staff the deployments and, more to the point, the ownership to mandate from the top: rip out a process, cut the headcount, deploy the tech, no permission required. The Thrive Holdings and Long Lake types stay pointed at this because the AI trade is their entire reason for existing. A traditional PE shop says it wants to deploy AI, then the moment it gets hard it reaches back into the usual bag of financial-engineering tricks. The AI-native firm doesn’t own that bag. It has one move, which is why it actually makes it.

The labs are running the same play from the supply side: enormous deployment teams whose job is to get enterprises burning down token commits and ramping API consumption. Same motion, different P&L line.

So the question I keep circling: if the next decade of fortunes gets made deploying capability rather than inventing it, are you building the thing, or the company that installs it for everyone who can’t?

Deals I’m Watching

The labs both stood up PE-backed deployment JVs. Days apart.

Within a week of each other, OpenAI and Anthropic each announced enterprise-deployment ventures capitalized by private equity, both built on the forward-deployed-engineer model, both aimed at the work Accenture and McKinsey do today.

On May 4, Anthropic went in with Blackstone, Hellman & Friedman, and Goldman Sachs: a roughly $1.5B services firm with $300M each from Anthropic, Blackstone, and H&F, plus Apollo, General Atlantic, GIC, Leonard Green, and Sequoia behind it. The target is mid-size, PE-owned companies with no deployment talent of their own; the firm later bought AI engineering shop Fractional AI to build out its delivery muscle. A week later, on May 11, OpenAI went bigger and stranger with The Deployment Company, a venture valued around $10B and backed by $4B+ in committed capital, anchored by TPG with Brookfield, Advent, and Bain across 19 investors. OpenAI keeps super-voting control; the sponsors get a guaranteed 17.5% annual return over five years. Days later, OpenAI bought consulting shop Tomoro to staff it.

Read that structure again. OpenAI took the messy, high-variance work of enterprise AI deployment and wrapped it in a capped, fixed-yield instrument a pension fund can underwrite. The labs have decided the fastest road into the mid-market runs through PE portfolios: hundreds of companies a single GP can mandate from the top. This is “deployment is all you need,” capitalized as its own asset class, in public, by the people building the models. When the labs conclude the money is in the deployment, the argument is over.

Beacon Software Raises $225M Series C

Up in the big-thoughts section I argued AI-native PE would outrun the traditional kind for one reason: the AI trade is its entire reason for existing, so it makes the hard top-down moves instead of reaching for the old tricks. Beacon Software is that argument with a logo on it.

A few weeks back, Beacon announced it had raised a $225M Series C on the heels of a $250M B in November 2025. Beacon is a Toronto roll-up from ex-Instacart president Nilam Ganenthiran and ex-Sequoia partner Divya Gupta, and it buys exactly the businesses no one in venture would touch: niche vertical software and services for youth sports leagues, campgrounds, manufacturers, unions, construction firms. Then it embeds engineers and AI into each one and grows it. The team calls itself “anti-private equity,” and the numbers it quotes are operating numbers rather than the multiple-arbitrage kind: acquired companies improving their Rule of 40 by roughly 1,000 basis points (ten points) inside a year, a fresh acquisition every couple of weeks. Raising $225M seven months after a $250M round tells you two things: the pace of buying is the strategy, and the price has moved well into the billions.

Look at who keeps showing up on the cap tables. Beacon is a General Catalyst company. So is Crescendo, the AI-native call center GC backed early, which paired its own AI with the acquired support firm PartnerHero and charges by outcome instead of the hour, already worth around $500M. So is Long Lake, the GC roll-up vehicle that agreed in May to take Amex Global Business Travel private for $6.3B, the strategy’s biggest swing yet. One firm, three versions of the same bet: buy the boring business, or build a new one beside it, then point AI at the work the incumbents pay people to do. GC isn’t picking winners in the AI-services trade. It’s manufacturing them.

Old-line PE hunts like a bat: echolocating in the dark for cheap multiples, leverage, a cost-out story, never really seeing the business it’s buying. The AI-native version is the other instrument. It points light at the operation and rebuilds the actual work. Same prey, Main Street companies with sticky customers and tired software, but one navigates by debt and the other by deployment. My bet from up top holds. When the AI trade is your whole reason for being, you turn the lights on. When it’s a line item, you keep flying blind and call it strategy.

One More Thing

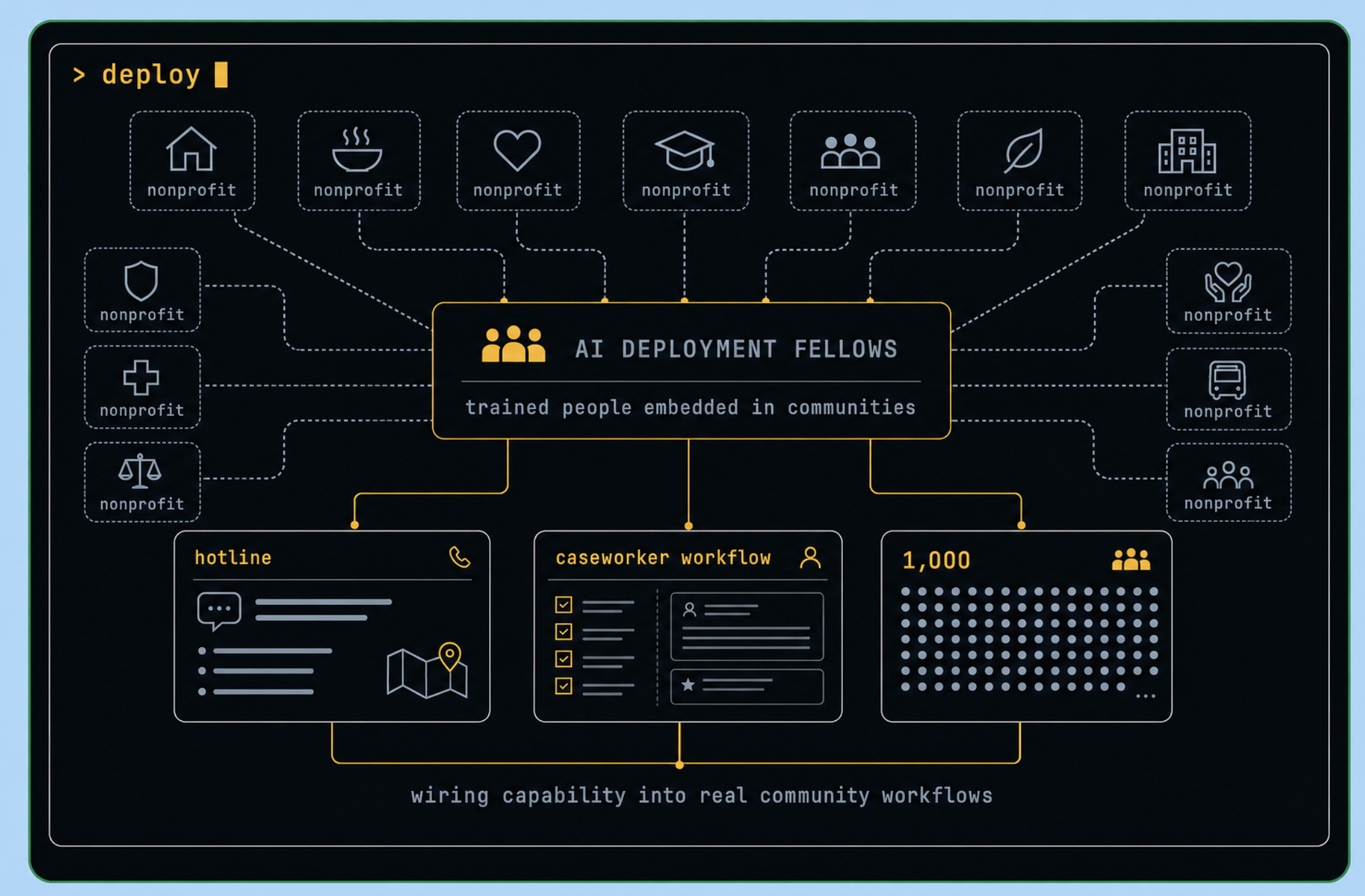

In June, Anthropic put up $150M for Claude Corps, a fellowship that trains 1,000 early-career people on AI and embeds them full-time inside US nonprofits for a year. Read it against everything above. It’s the same deployment motion the labs and the PE shops are running, just aimed at the part of the economy that will never raise a Series C. The capability has been sitting there for a while; what’s missing is someone in the building who can actually wire it in. I have some first-hand conviction here. I built NHV Navigator, a bilingual social-services directory and 24-hour hotline for New Haven, on nights and weekends with Claude doing most of the lifting, and the gap it closes for a caseworker or a family looking for a food pantry is immediate and real.

Now picture a thousand people doing that full-time, in a thousand organizations that could never afford a software team. If deployment is all you need, this is deployment pointed at the people who need it most. More of this, please.